Break-Down of Tax Reform Proposal

For businesses (directly from the articles linked below) –

- C Corporation Tax Rate and AMT: A measure to replace the current four-tier C corporation rates with a flat 20% rate (and a lower 25% rate for personal service corporations), and repeal the alternative minimum tax.

- New Pass-Through Entity Tax Rate: A portion of income from pass-through entities (i.e. sole proprietorships, partnerships, S corporations) would be taxed at a maximum rate of 25%, however this rate is not available to businesses involving the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees.

- Capital Expenditure Expensing: The bill would provide 100% expensing of qualified property acquired and placed in service after Sept. 27, 2017 and before Jan. 1, 2023. It would also increase (tenfold) the Sec. 179 expensing limitation ceiling and phaseout threshold to $5 million and $20 million, respectively, both indexed for inflation.

- Accounting Method Thresholds: The bill would increase the cash accounting method and percentage-of-completion method applicability thresholds.

- Net Operating Losses: Deductions of net operating losses (NOLs) would be limited to 90% of taxable income. NOLs would have an indefinite carryforward period, but carrybacks would no longer be available for most businesses.

- Like-Kind Exchanges: The bill would limit like-kind exchange treatment to real estate, but a transition rule would allow completion of currently pending like-kind exchanges of personal property.

- Deductions Eliminated: Deductions to be eliminated include entertainment, the domestic production activities deduction, and employee fringe benefits for transportation and certain other perks deemed personal in nature.

- Tax Credits Repealed: Credits repealed include the work opportunity credit, the credit for employer-provided child care, and the credit for rehabilitation of qualified buildings or certified historic structures.

- Foreign Provisions: The bill proposes several international tax changes including a repatriation provision—U.S. shareholders owning at least 10% of a foreign subsidiary will include in income the share of the post-1986 historical earnings and profits (E&P) of the foreign subsidiary, to the extent that E&P have not been previously subject to U.S. tax. The portion of E&P attributable to cash or cash equivalents would be taxed at a 12% rate and the remainder would be taxed at a 5% rate.

For individuals (directly from the article linked below) –

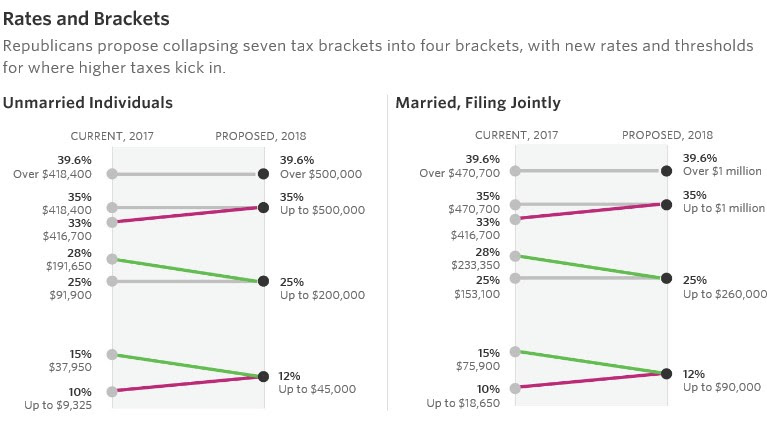

- Tax Rates: A measure to collapse the existing seven tax brackets into four tax brackets and increase the thresholds (see chart at the bottom).

- Alternative Minimum Tax: The bill would repeal the alternative minimum tax.

- Personal Exemptions and the Standard Deduction: Personal exemptions would be eliminated, but the standard deduction would increase from $6,350 to $12,200 for single taxpayers and from $12,700 to $24,400 for married couples filing jointly.

- State and Local Tax Deductions: The deduction for state and local income or sales taxes would be eliminated, except that income or sales taxes paid in carrying out a trade or business or producing income would still be deductible. State and local real property taxes would continue to be deductible, but only up to $10,000.

- Mortgage Interest Deduction: For newly purchased residences, the limit on deductibility of mortgage interest would be reduced to $500,000 of indebtedness from the current $1.1 million. Also, taxpayers would be limited to one qualified residence for purposes of the mortgage deduction.

- Deductions Eliminated: Deductions to be eliminated include alimony, student loan interest, tuition, moving, and itemized deductions such as medical, unreimbursed employee expenses, and tax preparation fees. However, the overall limitation imposed on itemized deductions (known as the “Pease limitation”) for certain higher income taxpayers would be repealed.

- Tax Credit Changes: Tax credit changes include the consolidation of existing education credits into one education credit capped at $2,500, an expanded child tax credit, and repeal of credits such as the plug-in electric vehicle credit and the adoption tax credit.

- Gain on Sale of Principal Residence: The exclusion of gain from the sale of a principal residence would be amended to require that the residence have been the taxpayer’s principal residence in five of the eight years preceding the sale. Taxpayers could use the exclusion only once every five years. The exclusion will phase out for taxpayers with modified adjusted gross income over $250,000 ($500,000 for married taxpayers filing a joint return).

- Education Savings Accounts: Contributions to Coverdell education savings accounts would be prohibited (except for rollovers), but taxpayers would be allowed to roll over money in their Coverdell ESAs into a Sec. 529 plan. Section 529 plans would be amended to allow limited distributions (up to $10,000) for elementary and secondary tuition.

- Estate Tax Phaseout: The estate tax would be repealed after 2023 (with the step-up in basis for inherited property retained). In the meantime, the estate tax exclusion amount would double (currently it is $5,490,000, indexed for inflation). The top gift tax rate would be lowered to 35%.

For more details, please refer to the following articles:

- Tax Reform General: https://www.thetaxadviser.com/

news/2017/nov/tax-reform-legis lation-details-201717798.html - Tax Reform for Individuals: https://www.thetaxadviser.com/

news/2017/nov/tax-reform-bill- changes-for-individuals-201717 806.html

Tax brackets chart published by the Wall Street Journal:

If you have questions or would like more information, contact an LCS&Z, L.L.P. advisor today!